Keeping family wealth and relationships in good shape

Keeping family wealth and relationships in good shape

The old saying “Shirtsleeves to shirtsleeves in three generations” means family wealth that’s built by the first generation is eroded or even destroyed by the third generation, which squanders the assets it inherits through reckless spending, poor investment decisions, and other mistakes.

The result: The family ends up back where it started, with the same amount of wealth (or less than) it began with generations ago. Unfortunately, it’s not just an adage.

We’ve seen this type of wealth destruction play out among many families—even those with relatively modest amounts of wealth—whose members tend to have their own conflicting agendas. They have (to varying degrees) different expectations, wants, and preferences. Moreover, there are commonly clashing perspectives on how best to manage and spend the family wealth. There may be family-owned business interests, and different family members may have differing ideas about the future of the company.

The good news: You can take steps right now that can potentially help you avoid watching your family’s wealth diminish over time—or stop you from being part of the problem. The key is to implement a process known as family governance.

Here’s how family governance works—and how it may help your family preserve, protect and grow its assets for generations to come.

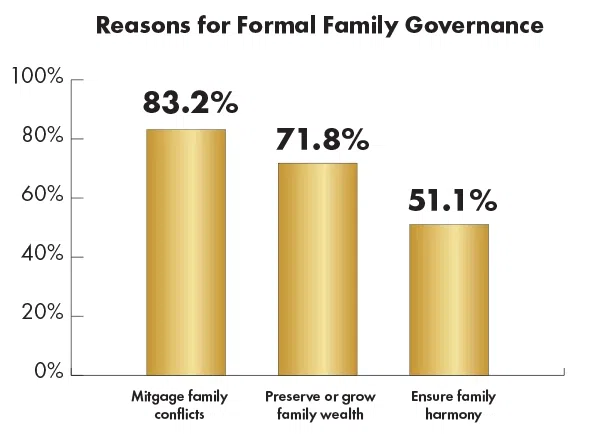

Formalizing family governance

Family governance at its core seeks to balance the competing needs of family members when there is substantial family wealth (and possibly business interests). But how family governance is structured can make a big difference. For example, addressing competing family members’ needs can happen by default without any real planning or formal structures. In such instances, control of the wealth is often concentrated in the hands of a matriarch or patriarch, or it changes as alliances among various family members, shift.

Or it can be done formally, by setting up approaches and controls designed to actively promote the betterment of the family overall. This is the approach we see affluent families take in most instances. The rationale for doing so is to inject some stability into the family’s wealth and potentially head off conflicts that might otherwise arise over money (see the chart).

Formal family governance has two core components: the human side and the technical side.

The human side tends to involve the steps taken to identify and create documents like mission statements/value statements and family constitutions. It is about developing a strong understanding of what the family is all about— including the roles and responsibilities of family members as a group and as individuals. Another aspect of the human side is specifying how family conflicts are to be resolved. The objectives are to avoid litigation and to make conflicts less intense and more manageable.

The technical side involves legal structures, which might include trusts, contracts (such as prenuptial agreements), partnerships, and corporate entities that officially codify the way family governance will work. In our experience, family dynamics almost always impact the types of legal structures a family chooses to implement for governance purposes.

Various professionals—including wealth managers, attorneys, and even family counselors—can potentially help families develop a formal family governance plan and help keep it on track.

Challenges in implementing family governance

With family governance, the biggest challenge is often following through on the plan and getting whatever model of governance you choose to work.

Consider how addressing only the human side of family governance can lead to problems. You could potentially spend lots of time and money on professionals to help you understand the wishes of family members and produce a mission statement, a values statement, and a comprehensive family constitution that includes a process for dispute resolution within the family. All the relevant family members might even formally sign on to these documents.

But when you pass away, your heirs could potentially jettison the agreed-upon approach and replace it with vicious litigation. With no formal legal documents in place, there’s no way to help ensure decisions will continue to be made in line with the family’s values.

Likewise, addressing only the technical side can result in problems down the line—as overly rigid documents and structures can lead to fights with trustees, lawsuits, and other problems for heirs.

The upshot: Lack of foresight when implementing formal plans can result in the headaches that family governance is intended to avoid. Typically, that occurs when families deal with only one aspect of governance instead of addressing the full range of issues needed to establish an effective family policy for the short and long term.

Building a solid plan

Family governance can be quite advantageous for family members. It can result in the further creation of wealth and the wise transfer of wealth from generation to generation. But to achieve these outcomes, family governance should be done thoughtfully and carefully—by both making a formal plan and then ensuring that plan adroitly combines the key human and technical aspects involved.

Next step: Contact your financial professional to discuss the various goals and objectives of your family members—and how a family governance plan could potentially help address family wealth and family harmony for years to come.

Keven P. Prather is a registered representative of and offers securities and investment advisory services through MML Investors Services, LLC. Member SIPC. Call 216-592-7314, send an email to kprather@financialguide.com or visit www.TransitioNextAdvisors.com for additional information.

Retirement looks relaxing, but many face loneliness, identity shifts and emotional stress. Here’s how to prepare now for a healthier transition.

Some common mental money mistakes

Master better decision-making with seven practical strategies that balance logic, intuition, and values for personal and professional success.

Discover what sets elite wealth managers apart—and how they deliver investment, planning, and personal value to affluent clients.

The deadline is approaching: key insights on understanding the CTA.