There are three liquidity ratios that answer the question, “Can I pay my bills?” They are the current ratio, the acid test, and the accounts receivable to accounts payable ratio. This month I’ll write about the third ratio: accounts receivable to accounts payable.

On the surface, this ratio seems straightforward: simply divide accounts receivable by accounts payable. However, if more than 50% of your business is COD, then the ratio must be calculated as accounts receivable plus cash divided by accounts payable. Why? If more than half of your revenues are paid in cash, you will receive the cash at the time of service or installation. Your bills to perform that service or installation are not due immediately. Usually you pay them in about 30 days, assuming you have credit with your suppliers. Therefore, you get the cash before you need to pay for the parts and equipment used on those jobs. You need to make sure that cash is there when the bills are due.

From a mathematical perspective, if your company is 100% COD or close to COD, then your receivables are zero or close to zero. When you divide by payables, the number is zero. This doesn’t make sense because unless you pay your bills COD, you have payables that must be paid.

Like the other liquidity ratios, it is the trends that are important. However, the trend interpretation is dependent on the receivable days trend, which I will discuss in a later column.

If the receivable days are constant, an increasing accounts receivable to accounts payable ratio means that profitability is increasing. If receivable days are increasing, then an increasing accounts receivable to accounts payable ratio means that you have a collection problem.

If the receivable days are constant, a decreasing accounts receivable to accounts payable ratio means that profitability is decreasing. If receivable days are decreasing, then a decreasing accounts receivable to accounts payable ratio means that your collection problem is decreasing.

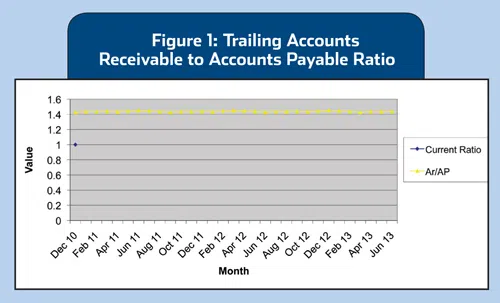

The best way to look at the trends is to plot the ratios. Figure 1 shows the trailing ratio or long-term view of a contractor who has a stable accounts receivable to accounts payable ratio. The company is collecting its revenues and paying its bills on a consistent basis. Profitability is constant.

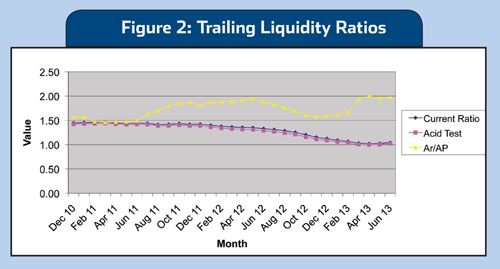

Figure 2 shows a contractor whose profitability is decreasing (current ratio and acid test are declining). The company also has very little inventory (as seen by the current ratio and acid test being close to each other). It also has collection problems at times. When the accounts receivable to accounts payable line is increasing with decreasing profitability, it is taking longer to collect revenues. Telephone calls must be made to decrease the collection issues.

An increasing accounts receivable to accounts payable ratio can have two messages. It might mean increasing profitability. It might mean you have a collection problem. Find out which is appropriate in your company.

Ruth King has over 25 years of experience in the hvacr industry and has worked with contractors, distributors, and manufacturers to help grow their companies and become more profitable. She is president of HVAC Channel TV and holds a Class II (unrestricted) contractors license in Georgia. Ruth has written two books: The Ugly Truth About Small Business and The Ugly Truth About Managing People. Contact Ruth at ruthking@hvacchannel.tv or 770.729.0258.

It’s all about negative accounts payable and negative credit cards payable.

Get the Insider Take on Mistake No. 6, Negative Accounts Receivable and Mistake No. 7 Negative Inventory.

Never Forget the Dangers of Negative Cash.

Explore Part 4 of the most common financial mistakes.

The mistakes to avoid when selling your business.