HVACR contractors who operate with divisions — whether it's two or 10 — and internally report net profit results for each division have a common problem. The question always is this: how to properly allocate expenses.

My first contracting company grew into a very large company with several distinct divisions. Every month when the company's financial results were issued to the division managers the debates began — better described often as arguments. Sometimes, heated arguments. I have no idea how much time and energy was consumed over this matter.

The situation really surfaced during our off-site monthly management meetings attended by seven managers and myself who facilitated the sessions.

Very importantly, there was a second problem. Managers who felt that allocations treated their division unfairly used allocation as a reason for their financial results not being as good as expected. They dodged accountability. You may be familiar with some of the managers' questions and statements I had to contend with:

In my consulting work I see many contractors dealing with the same allocation issues I've described. We solved the challenge many years ago by implementing a different financial reporting method — margin contribution accounting. Only then did the division managers begin accepting the financial results.

The other HVACR contracting companies I later owned operated on our new (at that time) reporting method. Several consulting clients have adopted this method.

In the margin contribution accounting method there is no allocation. As an example, let's use a company with four divisions: residential retail, residential new construction, commercial new construction and administrative. The first three divisions' (residential retail, residential new construction and commercial new construction) budgets and results are reported as revenues, cost of sales and gross profit as normally done.

To get the final divisional results, only the divisional overhead expenses are recognized with no allocation of administrative expenses. This results in not a divisional net profit, but instead a divisional margin contribution. This means that there are no debatable expenses. It also means, of course, that for those three mentioned divisions the margin contribution numbers are larger than previously used net profit numbers. Where a division that was previously allocated administrative expenses may have budgeted a net profit of 8 percent, it may now be budgeting a margin contribution of 15 percent.

In the administrative division, the fourth and last example division, revenues are very limited to discounts earned, gain on sale of assets and few other items. There are no cost-ofsales items. Gross profit is the same as revenues.

All of the administrative expenses are listed, resulting in an administrative division margin contribution loss. Expenses normally include, among certain other items, administrative salaries and wages, utilities, telephone, internet, data processing, business insurance, rent, contributions, interest expense, licenses, maintenance and repair of buildings; as well as office and shop equipment, management meeting expenses, consulting, office supplies and postage, and dues and subscriptions. The related administrative division expenses are charged to this division just like the other three divisions and include items such as payroll taxes, vacations and holiday, training, travel and vehicle expense.

If you're not using margin contribution internal accounting I recommend that you seriously consider it. Eliminate wasted time and energy and drive non-debatable accountability of your division managers.

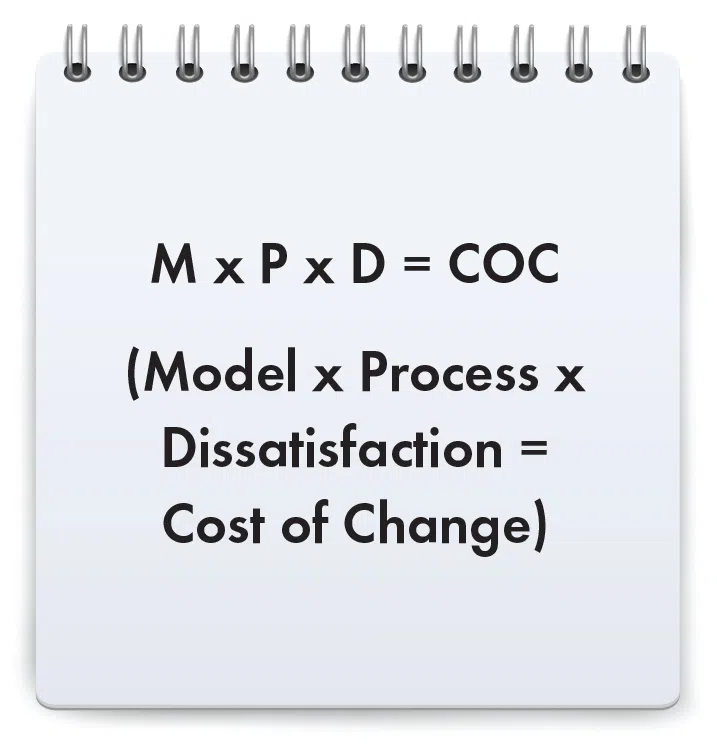

A Formula for Organizational Change

Building a highly profitable HVACR retail business with residential service agreements takes more than ideas, it takes proper training and execution.

.webp)

Start with a structured and organized approach. Make sure all owners buy into the program, your technicians are well-trained in performing quality precision tune-ups, and a process is established to …

Regardless of size and years of experience, certain information is appropriate for all contractors to define success.

Most everything changes and, often in a short period of time, changes again.